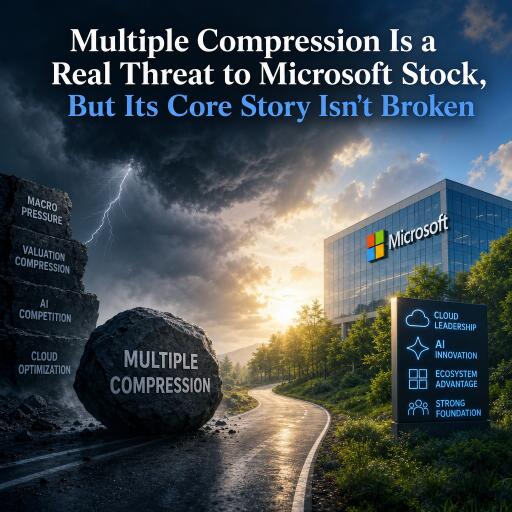

Multiple Compression Is a Real Threat to Microsoft Stock, But Its Core Story Isn’t Broken

The stock market for software plays started the year on a cautious note, with a broad technology fund sliding from its late-2025 highs and carving out a so‑called death cross as the 50‑day moving average slid under the 200‑day mark. That pattern helped sour sentiment and prompted some profit taking across the sector.

After years of exuberance fueled by AI hype, investors are confronting a more tempered reality. Many software groups acknowledge that weaving advanced AI features into products is expensive, and a sizable share—around seven in ten—say those costs are pressuring margins. The recalibration has rippled through the market, underscoring the fragility of lofty growth assumptions when profitability becomes harder to sustain.

Within this backdrop, a familiar name sits near the center of the adjustment: a major cloud and software powerhouse that accounts for roughly 8% of the sector’s benchmark software fund. The stock dipped about 10% on the heels of a solid earnings report that topped revenue and earnings expectations, even as investors focused on Azure’s growth deceleration—slowing from a previously brisk 40% pace to about 39%. The same dynamic surfaced again when a well-known research outfit trimmed its price outlook for the stock to the mid‑$500s range, citing ongoing multiple compression for software stocks even as it kept a constructive stance. Over the year, targets have been nudged downward in stages, reflecting a broader re-rating rather than a wholesale loss of confidence.

Are we witnessing a temporary pullback, or is this a more lasting shift in how investors value the company’s growth trajectory?

Assessing the Core Numbers Behind the Business

At its core, the company operates across a broad ecosystem: a cloud platform powering scalable services, a suite of productivity and collaboration tools, and a family of consumer- and enterprise-facing products—including a professional network, a dominant operating system, and a gaming franchise. The strength lies in durable, recurring revenue streams and a long-tail of enterprise customers that tend to stick with the platform over multiple years, even as market conditions wobble.

From a price‑action perspective, the stock has faced a substantial drawdown. It is down roughly a little over a fifth from its 52‑week high while recording a notable decline year to date. In valuation terms, the multiple has compressed toward peers, with forward earnings projecting a multiple in the low 20s. That sits in a more normalized zone after a long period of premium pricing, reflecting investors’ shift from “growth at any cost” to a steadier, cash‑generative profile.

On the income side, the dividend remains a feature of the story, though the yield sits below the broader tech average. Yet the payout has a long runway, with a history of annual increases extending over two decades, and a payout ratio in the low 20s, suggesting room to grow cash returns even as the growth narrative slows. The company continues to fund investments in cloud infrastructure and platform capabilities while returning capital to shareholders on a regular cadence.

From a gamer’s lens and a VR/AR observer’s view, the corporate strategy underscores a familiar tension: Microsoft’s gaming ambitions sit at a crossroads of hardware, subscription services, and cloud-enabled features such as live services and cross‑platform integrations. The resilience of the company’s cloud and productivity units supports a broader ecosystem that could help stabilize cash flow, even if near-term growth metrics in some segments show deceleration. In this light, the stock’s current price suggests the market is pricing in a slower ramp for some units, while remaining confident in the long‑term contribution from cloud, software, and platforms that tie together enterprise and consumer experiences.

In sum, the market appears to be recalibrating its expectations for near‑term growth while still acknowledging the company’s durable cash generation and diversified product mix. The path forward will likely hinge on how quickly cloud utilization returns to a steadier growth rate, whether new AI features manage to improve margins without eroding price discipline, and how gaming and related entertainment businesses contribute to overall profitability. If the growth re-acceleration proves elusive, the valuation could stay anchored at a more measured level; if it surprises to the upside, the multiple compression may begin to unwind.

For investors who navigate symphonies of platform value and recurring revenue, the core narrative remains compelling: a portfolio of high‑quality assets that together create a robust, if evolving, growth framework. While wall‑street consensus may push back on near‑term earnings multiples, the business’s long-run potential remains intact, anchored by enterprise demand, a scalable cloud backbone, and a steadfast commitment to shareholder returns.